IP Box is a preferential 5% tax rate for income from IP (copyrights and other intellectual property), applied only to so-called eligible income. The income is calculated using the Nexus index.

One of the most interesting tax credits is the so-called Innovation Box (also called IP Box). This preference allows you to cut down your tax rate to 5%! However, you must keep in mind that this does not apply to all income you earn, but only a fraction of it, called eligible income.

For more on how IP Box works, you can read my article: Innovation Box – 5% Income tax

IP BOX and eligible income

Eligible income equals your entire income from eligible intellectual property rights (for example copyrights to computer software) multiplied by the Nexus index.

If your research and development activities involve work on more than one eligible IP, in order to take advantage of IP Box you need to calculate the ratio separately for each eligible IP.

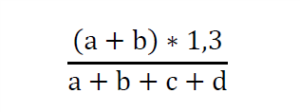

How to calculate the Nexus index?

Nexus is calculated according to the following formula:

Each letter below stands for costs actually incurred by the entrepreneur for:

a – directly conducted research and development activities related to a particular right;

b – acquiring the results of R&D works related to a particular right from unaffiliated entities;

c – acquiring the results of R&D works related to a particular right from affiliated entities;

d – acquiring an eligible intellectual property right.

In contrast to the R&D credit, provisions regulating IP Box do not list a closed set of eligible costs. The costs you incur should be classified as belonging to one of four groups marked with the letters a to d above.

How to account for employee and contractor remuneration when using the Nexus formula?

Costs resulting from an employment agreement can be classified as costs incurred for directly conducted R&D activities (letter a).

Remunerations of B2B contractors and associates, in turn, can be classified as acquiring the results of R&D works related to eligible IPs from an unaffiliated entity (letter b).

Expenses classified under a or b appear both in the formula’s numerator and denominator. This means that the manner of hiring workers who conduct R&D activities (employment agreement or contract to perform a specific activity) will not impact the Nexus index.

Nexus and costs of ‘own’ work

If you are a programmer or someone who works on a project on their own, most probably the sole cost you incur is the cost of your own work. According to regulations, such work is not treated as a tax cost, and therefore you cannot deduct it from your revenue. This does not mean, however, that you cannot become eligible for IP Box!

Moreover, according to explanations provided by the Ministry of Finance, the cost of your own work is not included when calculating the Nexus ratio.

In practice, this means you will not incur any costs of R&D activities.

How to calculate the Nexus index if you do not incur any costs of R&D activities?

The explanations above suggest that the index cannot be higher than 1. Otherwise, the amount of income from qualified IP when adjusted (multiplied) by the Nexus index would be higher than the income actually earned.

It was not explained, however, what ratio value should be applied if there are no costs to substitute in the Nexus formula. Calculating the index with zero costs of R&D activities would give a result of zero. Consequently, your income multiplied by the index would be zero as well, preventing your from taking advantage of IP Box in practice. You cannot divide by zero, after all!

Due to the lack of any regulations in this respect, we posed a question to the Director of the National Fiscal Information on behalf of one of our clients. As part of an application for individual interpretation we asked whether the Nexus formula could still apply if no costs were incurred for R&D activities other than the cost of own work. Should the ratio be equal to 1 as a result? In an individual interpretation obtained for our client (a programmer), the director of the NFI confirmed that in this situation, Nexus equals 1.

Thus, if you do not incur any costs of R&D activities and develop a product on your own, according to the position taken by the director of the NFI you can apply the maximum allowed index of 1. This means that your entire income from eligible IP rights is eligible income subject to the 5% tax rate.

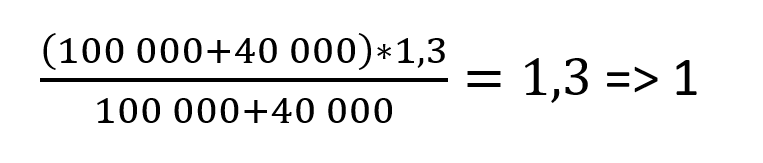

Example 1:

The taxpayer incurred PLN 140,000 in total expenses for R&D works on computer software, including:

- PLN 100,000 as direct expenses for R&D works (letter a, for example employee remuneration, equipment depreciation).

- PLN 40,000 as expenses to pay a research institute (letter b – expenses for an unaffiliated entity).

Calculating the index:

The Nexus ratio has been “cut down” to the maximum allowed value equal to 1.

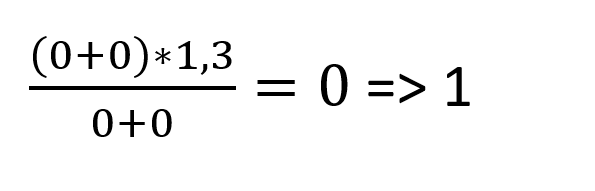

Example 2:

The taxpayer did not incur any costs of R&D activities except for costs of their own work which are not included in the calculation.

Calculating the ratio:

According to the interpretation obtained for our client, in this situation the ratio can be assumed to equal 1.

IMPORTANT INFO: Remember that individual interpretations affect only for the person who applied for them (hence the name). The position discussed above does not result directly from provisions of tax statutes or explanations of the Ministry of Finance. So, if you do not incur any costs of R&D activities and want to take advantage of IP Box, you should file an application for your own individual interpretation in order to be safe in case of a tax inspection.

***

Do you want to make sure you calculated the Nexus index correctly? Contact me at marcelina@msztax.pl

Are you a programmer? Do you want to know if you can apply for a 5% tax rate in Poland?

You can read my last article: Can a programmer benefit from IP box in Poland?